Almost everyone in America is for freedom and against dictatorship. The commitment varies from laissez faire advocates to progressives and all sorts of muddled preferences in-between. But it is a long held belief in this country that a government should respect the rights of individuals and not control their lives or their economies.

Now obviously different points of view exist. That’s why we have Democrats and Republicans. But no Democrat or Republican would stand before the American people and tell them that the economy should be run by the central government as it was under the Soviet Union, Communist China, Cuba, or the many other petty dictatorial regimes around the world, past or present.

The reasons most given for a free economy versus a controlled economy are two: one is on moral grounds. Freedom and the defense of basic human rights are moral while dictatorship and the enslavement of individuals is not. The other is on practical grounds. Free economies work and command economies do not.

There is not a single example that one can point to where a command economy, devoid of markets and freedoms, has enhanced the living standards of its citizens. But there are plenty of examples that show that increased freedoms and free markets do better than controls, regulations, and decrees. West Germany versus East Germany is one example. Communist China before increased freedoms and markets were allowed, and Communist China as a reformed economy after, is another.

Republicans are the party of more free markets and less government control over markets. Democrats are for more regulation of individuals, businesses, markets, and the economy in general.

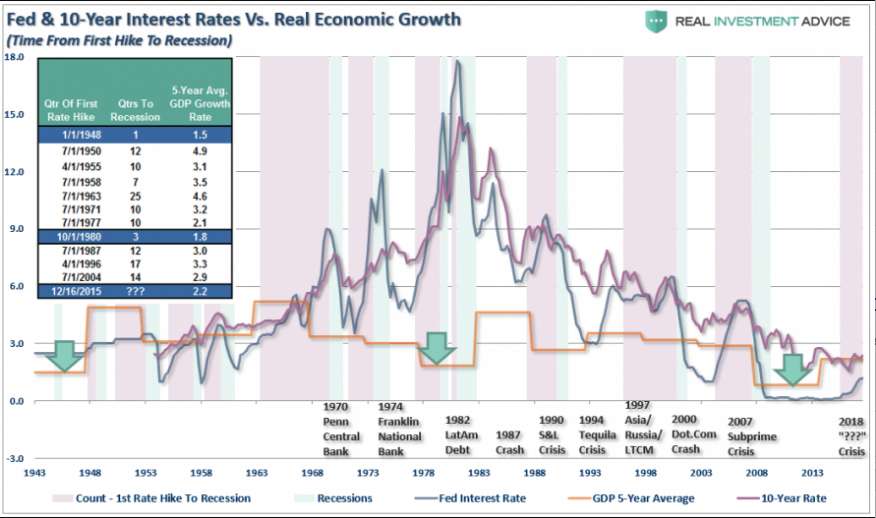

So I ask all Republicans, Conservatives, and Libertarians who value free markets, if a command economy doesn’t work, why do you think the Federal Reserve Board is or should be in control of interest rates? Even the Fed admits it lost control of interest rates years ago. Interest rates rose this year from 1.5% on the ten year bond to around 2.5%. Mortgage rates and a host of other rates followed. The Fed never raised interest rates. It never made a move. So who is really in control of interest rates, the Fed or the market?

Alan Greenspan recalls when the Fed decided to raise the fed funds rate a quarter percent at a time for over a year. He and all the Fed members were stunned when as they did so, the long term interest rates actually fell. That had never happen before. So again, who is in control?

Most of those on the Right and on the Left sincerely believe that the Fed controls interest rates–and they do, when it comes to the fed funds rate. But they do not control the price of money generally. So, If OPEC can’t control the price of oil, Japan can’t control its economy, and China can’t control its markets, why assume the Fed can control the price of money? Interest rates throughout the world are lower today than in all of history. That would be a victory for central banking if that were their goal. But their goal has been to raise growth rates and inflation rates; therefore interest rates should rise. Raising interest rates before growth and inflation rise is like putting the cart before the horse. Yet, this is called “normalization”, something they have yet been unable to do.

If price controls are futile as they always have been throughout history, why does the congress mandate that the fed funds rate be controlled by the Fed? Note that politicians, the Fed, and most economists and virtually all commentators today take it as a given that controlling the price of money is normal. They only talk about how interest rates should be controlled, not if they should be. Most talk about “normalizing” interest rates by decreeing higher rates. Why is an arbitrary higher rate normal, and a lower rate is not? The demand by the Right to raise interest rates is as irrational as the Left’s demands were in earlier times to lower interest rates. Why not let the market decide? The absence of a market driven interest rate is anti-free market.

Ben Bernanke, after leaving the Fed, admitted that the Fed generally follows market interest rates and that if they did nothing at all, interest rates would probably be little changed from where they are now. That totally contradicts the assumption that the Fed controls interest rates, and that the present interest rates are lower than they otherwise would be.

What this say’s to me is if the Fed let the Fed funds rate float and just maintained a reasonable money supply, interest rates would probably be about where they are today. An increase in the Fed funds rate would therefore be a Fed induced artificially high interest rate. Why would anyone for free markets want to decree a higher interest rate on a fragile economy especially when deflation and stagnation is the major threat that faces all nations?

Yet as commodity prices crash and world growth sinks, we hear the constant demand of the pundits, especially on the Right, urging us to raise interest rates now! Further they would like to tighten monetary policy by going to a “rule based” monetary policy — another policy based on decree rather than markets. The relentless attack by conservative politicians and commentators for the Fed to decree a tighter monetary policy is a glaring contradiction to free market economics. What they are asking for is to impose their theory over the verdict of the market.

The conflict amounts to a debate over whether a Monetary Rule or “discretion” should guide Fed monetary policy. Conservatives want either the Taylor Rule imposed, which would determine the level of interest rates by a mathematical formula, the return of the gold standard, which would impose monetary discipline, or a form of monetarism that fixes the rate of growth of the money supply.

The father of monetarism and foremost proponent of a rules based monetary policy, Milton Freidman, had an interesting view on this debate in a Wall Street Journal article from 2006:

“Over the course of a long friendship, Alan Greenspan and I have generally found ourselves in accord on monetary theory and policy, with one major exception. I have long favored the use of strict rules to control the amount of money created. Alan says I am wrong and that discretion is preferable, indeed essential. Now that his 18-year stint as chairman of the Fed is finished, I must confess that his performance has persuaded me that he is right—in his own case.

. . . It has long been an open question whether central banks have the technical ability to maintain stable prices. Their repeated failures to do so suggested that they did not — whence, in part, my preference for rigid rules. Alan Greenspan’s great achievement is to have demonstrated that it is possible to maintain stable prices. He has set a standard.”

Notice that Milton Freidman’s focus is on the Fed’s main mandate: maintaining stable prices. We do have, and have had stable prices for decades. So why this need, this demand, for a monetary rule? Inflation is not our problem. Paul Volker, Ben Bernanke, Janet Yellen, and a majority of Fed Members, (and I’ll bet Milton Freidman today if he were alive), agree that discretion is preferable to rules in today’s world. Yet in testimony in front of congress recently, Chair Yellen was constantly bombarded with questions and demands to move toward a rules-based policy, which she unambiguously and vehemently disagreed with. Why?

Isn’t it interesting that it is the Right that is for decreeing monetary policy, and the supposedly dictatorial Fed that is against such a policy and is in favor of following the market? After all, what does “data dependent” mean if not market dependent? The best monetary policy is a market oriented monetary policy based on market data, not some rule-based policy imposed by politicians or economists.

I am for allowing the Fed funds rate to float and seek its own level. This is a radical idea to most. However I believe that freedom is better than edicts, and that a Federal Reserve decreed interest rate is inferior to a market determined rate. All interest rates around the world are the lowest in history regardless of nation’s particular monetary policies. With quantitative easing or without it, interest rate levels for the world as a whole have not been this low in a thousand years. Certainly the market is trying to tell us something.

It’s time to consider the possibility that monetary conditions today are what they are, not because of central bank monetary policy — but in spite of it. The notion that the Fed can and should “normalize” interest rates by increasing them assumes that they know what “normal” is and are in control of the economy and of money. As we look around the world does anyone really believe that central banks are in control?

Perhaps it is not central bank monetary policies that control interest rates, but the demand for money. Note that US interest rates are about the same as they have been during years of money creation, and are about the same today without it. I agree with Ben Bernanke that if the Fed simply stepped aside, interest rates would be about the same as they are today without Fed intervention.

Rather than look to interest rates as a monetary tool, I suggest the opponents of the Fed, as well as the Fed itself, look toward understanding and fixing the all-time low velocity of money, the lack of loans being made, the reasons banks feel compelled to hold historically high levels of reserves rather than lend them out, the historically anemic economic growth and productivity rates, and address these problems rather than interest rate levels.

Fix the cause of these problems and maybe then we can return to normal. However it will take a lot more than the Fed to achieve that. It will take a reversion to fiscally conservative policies, deregulation, tax simplification, and a general move toward individual freedom, property rights, and free markets. It should also include re-defining the Feds mandate. The Fed’s job should be as lender of last resort and to ensure a stable price index. This is something the Fed has done and can do successfully. All other mandates are unworkable and therefore impracticle.

People need to stop wasting time attacking the Fed, and focus on the real enemy: the enemies of freedom and free markets. Only then will monetary stability and economic prosperity return.

For more discussion on this subject see the free commentaries at http://www.paulnathan.biz/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}